Automotive Human‑Machine Interface (HMI) Market is poised for significant growth—from approximately USD 23.5 billion in 2024 to an estimated USD 75.3 billion by 2033, reflecting a CAGR of around 12.3% ([turn0search3][turn0search2]). This surge is driven by increasing demand for seamless infotainment, voice and gesture controls, head-up displays, and multimodal digital cockpits in connected and autonomous vehicles.

Request Free Sample report:https://www.stellarmr.com/report/req_sample/Automotive-Human-Machine-Interface–HMI–Market/428

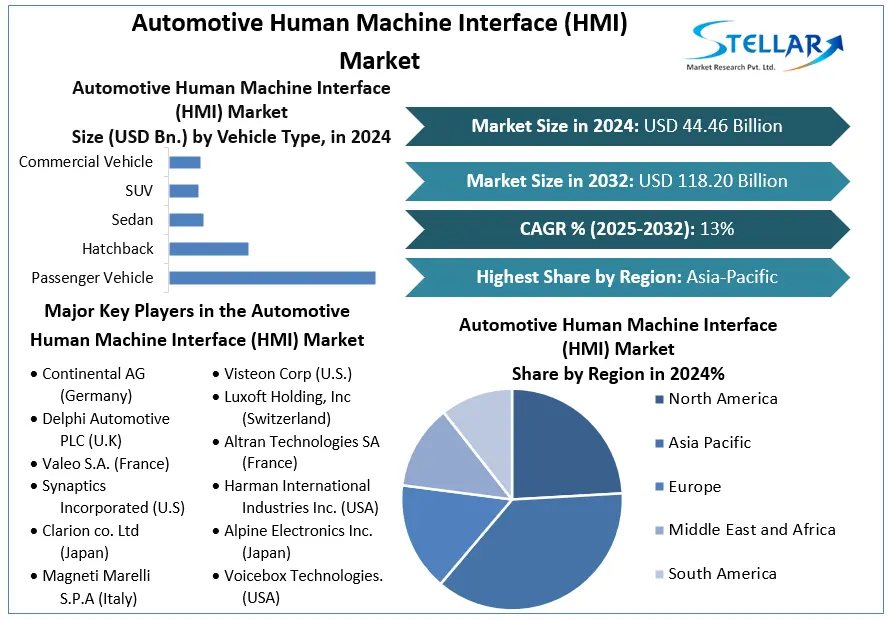

Market Estimation, Growth Drivers & Opportunities

The market size in 2023 hovered around USD 23.4–23.9 billion, growing to USD 40.2 billion by 2028 at ~11% CAGR ([turn0search8][turn0search9]). Updated forecasts show the industry reaching approximately USD 51.5 billion by 2033, with CAGR of 8.6% in some analyses ([turn0search2][turn0search3]).

Key growth drivers include:

-

Rising consumer expectations for intuitive interfaces in luxury and mainstream vehicles, including touchscreens, voice recognition, gesture control, and immersive HUDs.

-

ADAS and autonomous driving mandates, requiring clear, responsive HMI to communicate system status and facilitate handovers.

-

Software-defined vehicle architectures, unlocking OTA updates, subscription-based feature delivery, and cockpit personalization via AI integration.

-

Connected infotainment systems that combine cloud services, telematics, and safety alerts in real-time systems.

-

AI-driven UX innovations powered by generative AI, enabling new experiences inside the cockpit ([turn0search1][turn0search4]).

Opportunities span AR-enabled HUD development, voice‑AI copilots, gesture/eye tracking interaction, and premium user experiences in EVs and autonomous shuttles.

U.S. Market Trends & Investment

North America, led by the U.S., commands the largest regional share—valued at around USD 10.5 billion in 2024 ([turn0search10][turn0search2]).

Recent developments:

-

OEMs and suppliers are deploying AR-based head-up displays and multimodal systems combining touch, voice, and gesture for safer, immersive driving experiences.

-

Partnerships between OEMs and tech firms (like Qualcomm’s Snapdragon Digital Chassis being adopted by GM, Mercedes-Benz, and Stellantis) are enabling unified infotainment and HMI platforms ([turn0news12][turn0search2]).

-

Regulatory support for driver distraction mitigation—for example, NHTSA’s emphasis on intuitive cockpit interfaces—fuels adoption of advanced HMI designs ([turn0search1]).

Investment continues to flow into voice-AI enhancements, HUD pilots, and advanced interaction modalities tied to EV platforms.

Market Segmentation: Dominant Segment

Key segments of the market with largest share:

-

By Interface Type:

-

Touchscreens and instrument cluster displays held the largest share (~42% of revenue) in 2024, offering central functionality in infotainment and vehicle awareness ([turn0search1]).

-

Multimodal systems (combining voice, gesture, touch) captured ~51% of share in 2024 and are growing fastest (~14.8% CAGR) ([turn0search1][turn0search11]).

-

-

By Application:

-

Infotainment and navigation systems dominate, followed by ADAS-related displays, diagnostics, and personalized user controls ([turn0search11]).

-

-

By Vehicle Type:

-

Passenger vehicles, particularly luxury models, hold largest share in HMI adoption, while EVs grow fastest due to focus on digital cockpits ([turn0search8][turn0search1]).

-

-

By Region:

-

North America is the largest HMI market.

-

Asia-Pacific leads in adoption growth (~47.6% share in 2024) and is forecast fastest growing region through 2030–2033 ([turn0search1][turn0search5]).

-

Competitive Analysis: Top 5 Companies

Continental AG (Germany)

A leading supplier of HMI solutions including AR HUDs, gesture and voice systems. It collaborates with automakers like Hyundai to deliver high-performance cockpit interfaces ([turn0search0][turn0search6]).

Synaptics Incorporated (USA)

Provides touchscreen controllers and voice/gesture-recognition solutions embedded in digital dashboards and infotainment systems ([turn0search6][turn0search0]).

HARMAN International (USA) (Samsung subsidiary)

Supplies integrated infotainment and cockpit electronics platforms; expanding software-defined offerings with AI voice assistants and over-the-air UX upgrades.

Visteon Corporation (USA)

Designs cockpit electronics and cloud-connected HMI modules for major OEMs globally, focusing on digital cockpit deployments in EV models ([turn0search14]).

Luxoft / Aptiv

Luxoft provides HMI software development and integration services; Aptiv (Ireland) delivers end-to-end HMI hardware-software stacks to automakers across active safety and cockpit systems ([turn0search6][turn0search0]).

Other firms such as Valeo, Visteon, Alpine Electronics (Japan), Parrot Faurecia, Denso Ten, Tata Elxsi, and 3M contribute interface hardware, thermal displays, and UX development in various regions ([turn0search7][turn0search2]).

Regional Analysis: U.S., UK, Germany, France, Japan, China

-

United States (North America): Leading market due to rapid adoption of multimodal HMIs and deep integration of AI/UI systems in vehicle platforms; Qualcomm-powered digital chassis platforms are driving strategic HMI innovation ([turn0search2][turn0news12]).

-

Germany: Home to Continental and Bosch; strong industrial base for advanced HMI and HUD systems integrated into luxury European vehicle segments.

-

United Kingdom & France: Europe’s HMI innovation centers, with companies like Luxoft, Valeo, Parrot/Faurecia developing adaptive UIs, touchless controls, and connected cockpit software.

-

Japan: Led by Denso Ten, Alpine Electronics, and others, driving high-quality in-vehicle display systems, voice, and gesture controls for both domestic and export markets ([turn0search15][turn0search19]).

-

China (Asia‑Pacific): Largest regional market; aggressive RSUs and OEMs drive digital cockpit adoption, smart cluster displays, and voice-defined interfaces; APAC fastest-growing market forecast ([turn0search1][turn0search5]).

Conclusion

The Automotive HMI Market is on a robust trajectory—from USD 23.5 billion in 2024 toward USD 75.3 billion by 2033, expanding at approximately 12% CAGR. The trend is underpinned by consumer desire for immersive interfaces, regulatory emphasis on safe human–vehicle interaction, and transformation toward software-defined, connected automotive platforms.

Growth opportunities include:

-

Scaling multimodal interfaces that combine touch, voice, gesture, and AR displays.

-

Deploying AI-powered voice copilots and personalized UI across EVs and premium models.

-

Integrating AR-based HUDs with real-time safety alerts and navigation overlays.

-

Expanding OTA-capable HMI platforms enabling post-sale feature delivery and cockpit upgrades.

-

Focusing on Asia-Pacific expansion, where vehicle fleets and smart urban mobility demand advanced cockpit interfaces.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

sales@stellarmr.com