Crude Steel Market, valued at USD 1132.42 billion in 2023, is projected to reach USD 1477.24 billion by 2030, expanding at a CAGR of 3.9% during the forecast period. The growth is largely fueled by surging infrastructure development, expanding urbanization, and increasing steel consumption in renewable energy and automotive industries.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Crude-Steel–Market/934

Market Drivers and Opportunities

Crude steel is a foundational material used in construction, manufacturing, automotive, and energy sectors. The growing emphasis on infrastructure modernization across emerging and developed nations is a key growth driver. Additionally, the steel industry is evolving to align with global sustainability goals.

Key Growth Drivers:

-

Massive investments in infrastructure, transport networks, and housing.

-

Rising demand for electric vehicles (EVs) and lightweight high-strength steel.

-

Steel demand from renewable energy sectors, including wind turbine and solar farm installations.

-

Ongoing technological upgrades in steelmaking to reduce carbon emissions and improve efficiency.

Opportunities:

-

Expansion in developing nations like India and Southeast Asia.

-

Development of green steel technologies, including hydrogen-based steel production.

-

Growth in pre-engineered buildings and modular construction driving demand for structural steel.

U.S. Market Trends and Investment (2024 Update)

The U.S. steel industry is undergoing a significant transformation in 2024. Major players such as U.S. Steel, Nucor, and Cleveland-Cliffs have announced multi-billion-dollar investments in electric arc furnace (EAF) technology, aiming to reduce carbon emissions and align with net-zero goals. Additionally, federal infrastructure funding under the Infrastructure Investment and Jobs Act (IIJA) is accelerating demand for steel in bridges, roads, and rail.

There is a growing shift toward recycled steel and low-carbon steel solutions, and domestic steelmakers are collaborating with auto manufacturers to support the EV transition. The recent tariff revisions and efforts to enhance trade partnerships have also positively influenced the U.S. market.

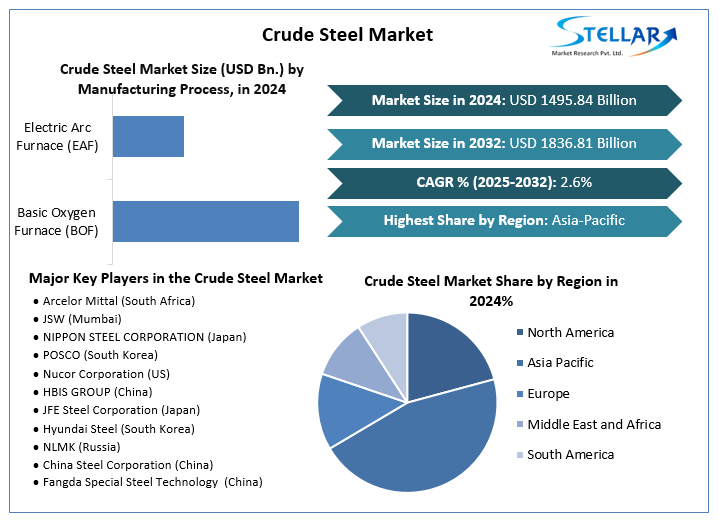

Market Segmentation: Leaders by Share

According to the segmentation in the report:

-

By Process, the Basic Oxygen Furnace (BOF) method holds the largest market share due to its high-volume production capacity and dominance in Asia.

-

By Application, the construction sector accounts for the largest share of crude steel consumption globally, driven by infrastructure and commercial projects.

Competitive Landscape

The global crude steel market is highly consolidated, with key players investing in innovation, sustainability, and capacity expansion. The top five players dominating the market include:

-

ArcelorMittal – World’s largest steelmaker focusing on decarbonized steelmaking, investing in DRI and hydrogen projects across Europe.

-

China Baowu Steel Group – Leading global producer expanding its smart steel plant capacity and exploring AI-driven manufacturing.

-

Nippon Steel Corporation – Recently committed to net-zero targets by 2050, with innovations in low-emission steel production.

-

HBIS Group – Focusing on ultra-low emissions, the company has launched China’s first hydrogen-fueled pilot steel project.

-

POSCO – Investing in hydrogen-based steelmaking and advanced automotive-grade steel, especially for EV manufacturers.

These companies are actively transforming their operations to align with green steel policies and digital transformation initiatives, significantly shaping the future of the global steel landscape.

Regional Insights

-

USA: Holds a significant share of the North American market. Supportive policies, infrastructure investments, and clean steel incentives are boosting domestic production.

-

UK: The British government has launched a £600 million support scheme for decarbonizing the steel sector, including transitioning to EAF technology.

-

Germany: Germany is leading Europe’s green steel movement with €2 billion funding support for clean steel production technologies.

-

France: Focused on nuclear and renewable infrastructure where steel demand is steadily increasing. Investments in rebar and structural steel production are ongoing.

-

Japan: Advanced steel technologies, robotics integration, and a focus on lightweight, high-performance steels are driving market growth.

-

China: Despite production caps due to environmental concerns, China remains the largest crude steel producer, supported by large-scale infrastructure, urbanization, and technological advancements in steel recycling and circular economy practices.

Conclusion

The global crude steel market is witnessing a steady but dynamic transformation. While traditional demand from infrastructure and construction remains robust, the shift toward green steel, recycled materials, and energy-efficient production is creating exciting new opportunities. With governments incentivizing sustainable practices and key players making strategic investments in innovation and clean technology, the market is well-positioned to grow sustainably.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

sales@stellarmr.com