Vascular Access Device Market: Enhancing Patient Care with Innovation and Reliability

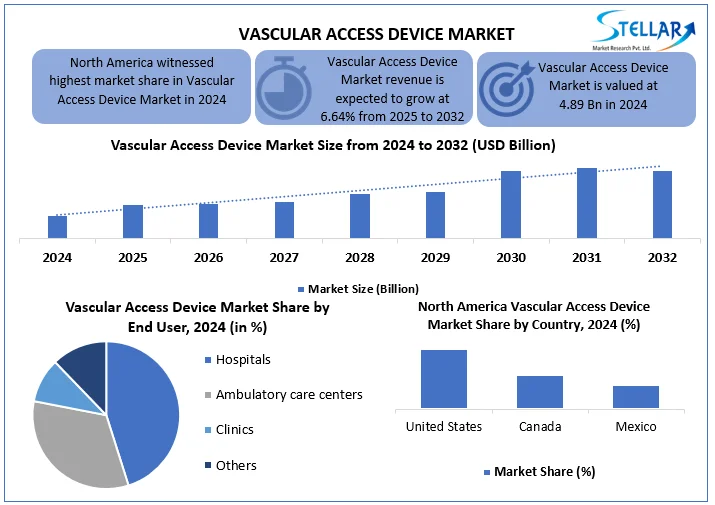

The Vascular Access Device Market is expanding steadily as healthcare systems worldwide respond to rising chronic disease prevalence, aging populations, and the increasing need for efficient intravenous therapies and minimally invasive procedures. In 2024, the market was valued at approximately USD 4.89 billion and is projected to grow at a compound annual growth rate (CAGR) of 6.64 % from 2024 to 2032, reaching nearly USD 8.18 billion. This growth reflects the widespread use of vascular access devices in hospitals, clinics, ambulatory centers, and home healthcare settings for drug delivery, fluid administration, diagnostic procedures, and long-term treatment regimens.

Request Free Sample Report : https://www.stellarmr.com/report/req_sample/vascular-access-device-market/2594

Market Estimation & Definition

Vascular access devices (VADs) are medical tools used to gain reliable entry into the vascular system for therapeutic, diagnostic, and monitoring purposes. These devices include peripheral intravenous catheters (PIVCs), central venous catheters (CVCs), peripherally inserted central catheters (PICCs), midline catheters, Huber needles, and other specialized access tools. Their key function is to facilitate safe and effective delivery of medications, fluids, nutrition, and blood products directly into a patient’s bloodstream while minimizing patient discomfort and procedural complications.

Reliable vascular access is essential in various clinical scenarios — ranging from emergency care and intensive treatments to chronic disease management and routine diagnostic testing — making VADs integral to modern healthcare delivery.

Market Growth Drivers & Opportunity

A primary driver of market growth is the rising prevalence of chronic diseases such as cancer, cardiovascular disorders, diabetes, and kidney disease. These conditions often require long-term intravenous therapy, repeated blood sampling, chemotherapy, dialysis, and fluid administration — all of which depend on vascular access devices. With chronic diseases accounting for a growing share of global morbidity, demand for VADs continues to rise.

The aging global population is another key factor. Older adults are more likely to experience conditions that necessitate frequent hospital admissions and prolonged treatment regimens, further increasing the need for dependable vascular access solutions. Between 2015 and 2050, the proportion of people aged 60 and above is expected to nearly double — a demographic shift that strongly supports long-term demand for vascular access technologies.

Technological advancements and product innovations also present significant opportunities. Improved catheter designs, antimicrobial coatings, hypoallergenic materials, and ultrasound-guided insertion systems are reducing infection risks and procedural complications. These innovations enhance patient safety and expand the clinical utility of vascular access devices.

Additionally, the shift toward home-based care and outpatient treatment models is driving demand for portable, easy-to-use VADs. Patients receiving long-term therapies at home — such as parenteral nutrition, antibiotic regimens, and pain management — increasingly rely on advanced access solutions to maintain comfort and treatment continuity outside hospital environments.

Request Free Sample Report : https://www.stellarmr.com/report/req_sample/vascular-access-device-market/2594

What Lies Ahead: Emerging Trends Shaping the Future

Several trends are shaping the evolution of the Vascular Access Device Market:

-

Smart and Connected Devices: Integration of digital sensors and wireless technologies enables real-time monitoring of catheter performance, flow rates, and early detection of complications, allowing clinicians to intervene proactively and improve patient outcomes.

-

Ultrasound-Guided and Image-Assisted Solutions: Increased adoption of image-guided placement techniques improves first-attempt success rates and reduces procedural complications, especially in populations with difficult vascular access.

-

Antimicrobial and Anti-Thrombogenic Technologies: The use of antimicrobial coatings and advanced materials reduces infection risks, one of the most significant challenges in vascular access procedures, and enhances device longevity and safety.

-

Growth in Outpatient and Ambulatory Care: With healthcare systems emphasizing cost-effective, patient-centered care, the demand for VADs in ambulatory surgical centers and outpatient clinics is rising, driven by shorter hospital stays and expanding preventive care models.

These trends reflect the market’s shift from traditional devices to intelligent, safer, and more adaptable solutions.

Segmentation Analysis

The vascular access device market is segmented primarily by product type and end user:

-

By Product Type:

-

Short PIVCs (Peripheral Intravenous Catheters)

-

Huber Needles

-

Midline Catheters

-

PICCs (Peripherally Inserted Central Catheters)

-

CVCs (Central Venous Catheters)

-

Others

Short PIVCs currently dominate due to their widespread use in hospitals, emergency units, and general clinical environments. Their ease of insertion, low cost, and versatility make them the most commonly deployed vascular access solution.

-

-

By End User:

-

Hospitals

-

Ambulatory Care Centers

-

Clinics

-

Others

Hospitals represent the largest end-user segment, driven by high volumes of surgical procedures, inpatient care services, and chronic disease management activities that require frequent vascular access.

-

Country-Level Analysis: USA & Germany

In the United States, the VAD market benefits from a well-developed healthcare infrastructure, strong healthcare spending, and high adoption of advanced medical technologies. The U.S. leads globally in the use of VAD innovations such as antimicrobial catheters, ultrasound-guided placement systems, and smart monitoring tools. The prevalence of cancer and chronic kidney disease in the U.S. further fuels demand for reliable vascular access solutions in both inpatient and home care settings.

In Germany, a leading healthcare market in Europe with stringent safety standards and strong medical device regulations, VAD adoption is supported by high clinical care quality and continued innovation. German healthcare providers emphasize patient safety and infection control, driving uptake of advanced catheters and vascular access technologies in hospitals, outpatient facilities, and specialized clinics. Germany’s aging population and chronic disease burden reinforce the need for effective vascular access solutions.

Competitor Analysis

The vascular access device market is competitive and includes several global leaders and specialized manufacturers. Key players include B. Braun Melsungen AG (Germany), Coloplast A/S (Denmark), Terumo Corporation (Japan), Becton, Dickinson and Company (USA), Medtronic, Edwards Lifesciences, ICU Medical, Teleflex, AngioDynamics, Cook Medical, and healthcare technology firms such as Fresenius Medical Care and Siemens Healthineers. These companies prioritize product innovation, quality, infection-reducing technologies, and global distribution networks to capture market share and address clinical needs across different care settings.

Conclusion

The Vascular Access Device Market is on a positive trajectory, driven by increasing chronic disease prevalence, technological innovations, expanding ambulatory care models, and an aging global population. As healthcare continues to evolve with smarter, safer, and more patient-centric solutions, vascular access devices will remain vital tools in clinical practice — supporting efficient drug delivery, fluid management, diagnostic procedures, and long-term treatment regimens. With advances in antimicrobial designs, image-guided systems, and smart monitoring technologies, the market is poised to deliver better outcomes, enhanced safety, and improved quality of life for patients worldwide.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com