Marine Urea Market: Global Growth, Regulatory Drivers, and Future Trends

Market Estimation & Definition

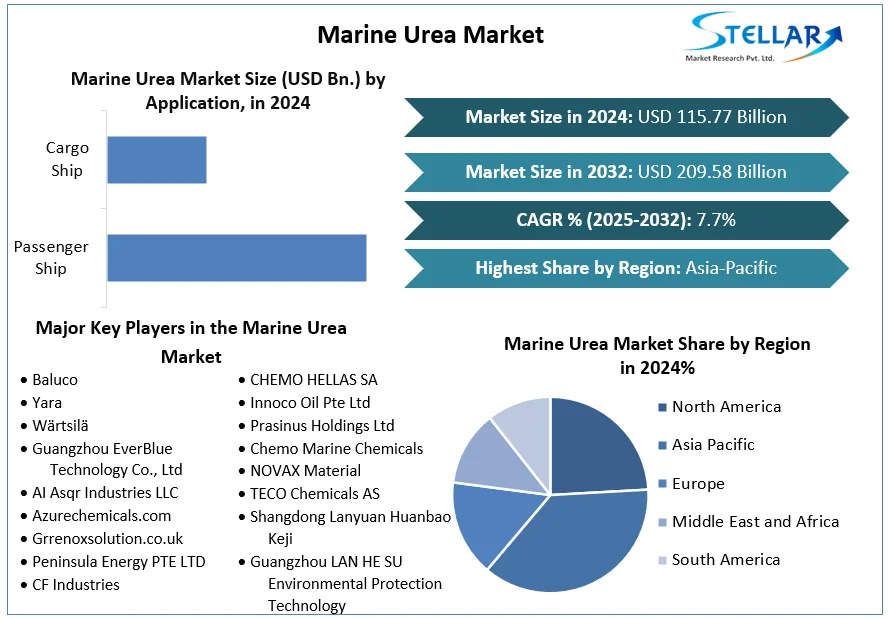

The marine urea market refers to the global industry for marine‑grade urea solutions, commonly known as AUS 40 — a 39%‑41% aqueous urea solution used primarily in Selective Catalytic Reduction (SCR) systems aboard ships to curb nitrogen oxide (NOx) emissions from diesel engines. This product reacts with NOx gases in vessel exhausts to form harmless nitrogen and water, aiding compliance with international maritime environmental standards and improving air quality. The market was valued at approximately USD 115.77 billion in 2024 and is projected to reach roughly USD 209.58 billion by 2032, growing at a CAGR of around 7.7 % over the forecast period.

Purchase This Research Report at up to 30% Off @ https://www.stellarmr.com/report/req_sample/marine-urea-market/2460

Market Growth Drivers & Opportunity

The marine urea market is driven significantly by stringent regulatory mandates aimed at reducing marine emissions. The International Maritime Organization’s (IMO) Tier III regulations under MARPOL Annex VI require up to 60‑70 % reduction in NOx emissions from ships operating in designated Emission Control Areas (ECAs). Compliance with these standards has accelerated Selective Catalytic Reduction (SCR) adoption on new vessels and retrofitted fleets, boosting demand for AUS 40 solutions.

Global trade expansion and the corresponding increase in shipping activity — cargo carriers, cruise liners, and container vessels — further support market growth. A larger fleet inevitably produces more emissions, prompting broader implementation of emission control technologies that depend on marine urea for operation. As environmental awareness continues to grow among operators and regulators, the pressure to deploy clean maritime technologies creates ongoing opportunity for market expansion.

In addition, technological advances in SCR systems and optimized urea dosing and monitoring solutions present opportunities for improved performance and reduced operational costs, making marine urea increasingly attractive to shipping companies and port service providers.

What Lies Ahead: Emerging Trends Shaping the Future

Looking ahead, integration of digital and IoT‑enabled technologies in SCR systems is emerging as a key trend. Remote monitoring and automated dosing can enhance urea consumption efficiency and reduce maintenance downtime, which is critical for operators seeking both environmental compliance and cost control.

Another trend is standardization of high‑purity AUS 40 solutions with stringent ISO compliance and lower impurity levels, enabling better performance and longer storage stability. This aligns with maritime operators’ needs for more reliable and consistent emissions control under diverse operational conditions.

Additionally, the expansion of emission control zones (ECAs) beyond traditional areas such as North America and Northern Europe to other global regions will continue to propel adoption of marine urea, extending demand into developing maritime markets.

Purchase This Research Report at up to 30% Off @ https://www.stellarmr.com/report/req_sample/marine-urea-market/2460

Segmentation Analysis from the URL

The marine urea market is segmented based on type and application:

By Type:

• 39%‑40% concentration – Widely used due to optimal NOx reduction effectiveness and easier handling characteristics.

• 40%‑41% concentration – Used for more stringent regulatory compliance, particularly in regions with aggressive emission standards.

By Application:

• Passenger Ships – Dominant due to frequent operations within Emission Control Areas and high environmental scrutiny.

• Cargo Ships – Fastest‑growing segment as stricter regulations push retrofit and new SCR adoption across commercial fleets.

• Other Vessels – Includes smaller marine vessels and support crafts that also adopt SCR technology to meet local emission norms.

Country‑Level Analysis — USA and Germany

In the United States, the marine urea market is influenced by strict regional environmental regulations along coastal ECAs (such as those in the U.S. Caribbean Sea and coastal California) that require significant NOx reductions from vessels. This has encouraged SCR system adoption across commercial fleets and expanded AUS 40 bunkering infrastructure at key ports, contributing to rapid market growth.

In Germany, part of the European Union’s Northern and Baltic Sea ECAs, high SCR penetration reflects rigorous emission controls and strong compliance enforcement. German operators and ports such as Hamburg and Bremen have reported consistent increases in marine urea consumption, driven by both domestic regulatory frameworks and broader EU environmental commitments.

Commutator Analysis

The competitive landscape is marked by a mix of global chemical suppliers, maritime bunkering specialists, and industrial solution providers. Key players include Baluco, Yara, Wärtsilä, Guangzhou EverBlue Technology Co., AI Asqr Industries LLC, Azurechemicals.com, and Grrenoxsolution.co.uk, alongside several regional and niche manufacturers. These companies compete based on product quality, supply reliability, global distribution networks, and technical support for SCR technologies.

Leading firms are enhancing their market positioning through expanded production capacity, partnerships with shipping operators, and services that support on‑board handling and infrastructure at major ports worldwide. Robust logistics and flexible supply options are increasingly important to address supply chain volatility and port‑specific requirements.

Press Release Conclusion

The marine urea market stands at the forefront of the maritime industry’s transition toward cleaner operations and stricter emissions compliance. Driven by regulatory mandates, expanded shipping activities, and technological innovation in emissions control systems, the marine urea sector is projected to sustain strong growth through 2032. With key markets such as the United States and Germany enforcing stringent NOx reduction standards, and emerging regions adopting similar rules, demand for high‑quality AUS 40 solutions will continue to rise. Stakeholders that prioritize technological enhancements, robust supply chains, and strategic global partnerships are well positioned to capitalize on this dynamic and environmentally critical market.

About Us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com