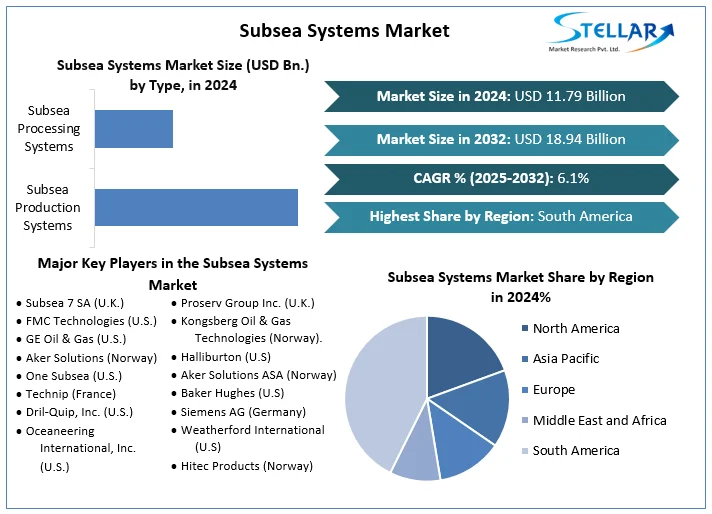

Subsea Systems Market is experiencing robust growth, with its valuation expected to climb from approximately USD 13.2 billion in 2023 to around USD 20.7 billion by 2032, registering a CAGR of 5.8% during the forecast period. This growth is primarily driven by expanding offshore exploration activities, increasing investments in subsea cable infrastructure, and a strong push towards renewable energy development.

Request Free Sample Report:https://www.stellarmr.com/report/req_sample/Subsea-Systems-Market/357

Market Estimation, Growth Drivers & Opportunities

Subsea systems play a crucial role in offshore oil & gas production and renewable energy transmission. They include technologies like subsea production systems, processing systems, and SURF (Subsea Umbilicals, Risers, and Flowlines) infrastructure.

Key growth drivers include:

-

Increased Offshore Oil & Gas Exploration: Depleting onshore reserves are pushing operators toward deepwater and ultra-deepwater fields, especially in regions like the Gulf of Mexico, Brazil, West Africa, and Southeast Asia. These environments rely heavily on subsea technologies for safe and efficient extraction.

-

Rising Demand for Subsea Communication and Power Cables: The surge in global internet connectivity, data centers, and cloud computing is fueling demand for subsea fiber optic cables. Additionally, offshore wind farms are driving growth in subsea power cables and connectors.

-

Advancements in Subsea Technologies: Companies are investing in smart subsea systems featuring digital twin technology, predictive maintenance, and real-time monitoring, which enhance operational efficiency and reduce downtime.

-

Government Support & Global Energy Transition: Many governments are backing offshore wind and subsea power cable projects to achieve energy security and net-zero targets, creating substantial opportunities for subsea infrastructure suppliers.

U.S. Market Trends and Investment Scenario

The United States continues to be a dominant player in the subsea systems market, primarily due to ongoing deepwater oil & gas activities in the Gulf of Mexico. U.S. oil majors and independents are deploying advanced subsea production and boosting systems to extend field life and enhance recovery rates.

Recent developments have also highlighted a shift towards subsea cable investments, particularly from technology companies. Firms such as Meta and Google are investing in extensive undersea cable networks to support AI infrastructure, driving demand for advanced subsea cable-laying technologies and services.

The Biden administration’s push for offshore wind power, with targets of deploying 30 GW by 2030, is further boosting demand for subsea transmission systems along the U.S. East Coast.

Market Segmentation: Key Highlights

By Type:

-

Subsea Production Systems dominate the market, accounting for the largest share. These systems include subsea trees, manifolds, and templates and are critical in complex offshore oilfield developments.

-

Subsea Processing Systems are gaining traction due to their role in enhancing oil recovery and enabling longer tiebacks.

By Component:

-

The SURF segment (Subsea Umbilicals, Risers, and Flowlines) holds significant market share due to the infrastructure’s essential function in fluid transport and control between subsea equipment and surface facilities.

By Application:

-

Offshore Oil & Gas remains the largest application area.

-

However, Renewable Energy applications such as offshore wind farms are expected to see the fastest growth over the forecast period.

Competitive Landscape: Top 5 Companies

The Subsea Systems Market is highly competitive and dominated by leading players with global operations and extensive project portfolios.

1. Subsea 7 S.A.

Headquartered in the UK, Subsea 7 specializes in subsea engineering and construction services, particularly in SURF systems. The company has a robust presence in deepwater projects across Europe, Africa, and the Americas.

2. TechnipFMC plc

This French-American company is a pioneer in subsea production and processing systems. It continues to innovate in integrated subsea engineering solutions, including compact manifold systems and subsea boosting technologies.

3. OneSubsea (SLB, Aker Solutions, Subsea 7 JV)

This strategic joint venture combines the technical expertise and resources of three leading subsea companies, offering highly integrated subsea production and processing solutions. OneSubsea is known for its high-capacity subsea pumps and digital controls.

4. Oceaneering International, Inc.

Based in the U.S., Oceaneering provides ROVs, subsea hardware, asset integrity, and field support services. Its diversified subsea offerings support both oil & gas and renewable energy projects globally.

5. Aker Solutions ASA

A Norway-based engineering company, Aker Solutions is a key player in the manufacturing of subsea production systems. The company’s focus on modularization and standardization has helped reduce project lead times and costs.

These companies are actively investing in R&D to enhance automation, system reliability, and digital integration, which are becoming increasingly essential in modern subsea operations.

Regional Insights

United States:

The Gulf of Mexico continues to be a hotbed for subsea investments. Government incentives for offshore wind projects are also pushing the adoption of subsea cables and supporting equipment on the Atlantic coast.

United Kingdom:

The UK North Sea is transitioning from oil & gas to offshore wind, with major investments in subsea power cables and connectors. Scotland and the North Sea are home to large-scale floating wind projects requiring advanced subsea infrastructure.

Germany and France:

These countries are focusing on energy transition and offshore wind energy, leading to growing demand for subsea cable solutions and connectors. Government support is fostering new investments in subsea systems for green energy deployment.

Japan:

Japan is investing in offshore wind energy and seismic monitoring cables, with a focus on disaster resilience. These applications require specialized subsea systems for power and communication transmission.

China:

China is aggressively expanding its offshore wind capacity and undersea data cable infrastructure. With local players increasing manufacturing capabilities, the country is becoming a key regional contributor to the global subsea market.

Conclusion

The Subsea Systems Market is poised for significant growth driven by deepwater oilfield developments, surging investments in offshore renewable energy, and global data infrastructure expansion. Companies offering integrated, digital, and energy-efficient subsea systems will be best positioned to capitalize on these trends.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

+91 9607365656

sales@stellarmr.com